What is Mortgage Insurance?

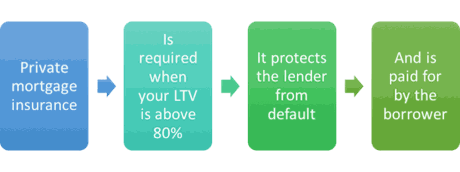

When obtaining a mortgage for a home and if a buyer has less than 20% down payment, mortgage insurance is generally required to protect the lender in the event the borrower defaults on the loan. Private Mortgage Insurance (PMI) is applied to non-government loans and Mortgage Insurance Premium (MIP), is applied to government loans. VA loans are the exception to the rule and has no mortgage insurance.

Payment

Payment

Depending on the loan, premiums can be paid in full up front, a portion paid upfront along with a smaller monthly premium, or the premium can be paid monthly. Another way of paying for the mortgage insurance is to have the lender pay for it by increasing the interest rate. The better the credit score and the greater the down payment the premium will be less.

If there is a monthly PMI payment, it is paid at the time when the mortgage payment is due and the borrower makes one payment consisting of PITI (principal, interest, property taxes, and homeowner’s insurance) and PMI/MIP. Keep in mind homeowner’s insurance protects the physical home and property liability while PMI protects the lender from borrower default.

Cost of mortgage insurance

A rule of thumb might be a range of $30-100 per month for every $100,000 borrowed or nothing at all if the premium is paid in full upfront. With decent credit scores and 5-10% down payment, the borrower can expect a breakeven for the policy after 3-4 years of mortgage payments if the premium is paid upfront. Marginal credit scores will drive the cost of the premium higher and breakeven will take longer.

Removing PMI

PMI can be dropped from the loan. To eliminate PMI, if the borrower can demonstrate 20% equity (usually by way of an appraisal), or if there is 22% equity (generally based on the original purchase appraisal and drops automatically) in the home, the insurance can be removed. Some lenders require seasoning of the loan as well. Borrowers also have the option of refinancing the loan and the insurance may be dropped provided there is 20% equity. With government loans, the MIP will stay for the life of the loan. PMI does not help build equity and provides additional motivation to remove it.

![]()

Quick Property Search

Useful Information Buyers and Sellers

Search for Homes South King County

Search for Homes Pierce County