Let’s Talk Credit Scores

As much as we try to eliminate debt, credit scores are based on getting into debt! Establishing a credit score will take time and careful management of debt. Having a good mixture of credit, paying debt on time with conservative balances relative to credit limits will drive your scores higher. What hurts credit scores? Missing a payment that is reported to the bureaus is a deathblow. Having a foreclosure, car repossession, and many other factors will also drop your scores. With patience, low scores can be reversed by better management of debt. Improving credit scores begins with lessening the balances on your accounts and making payments on a timely basis. From a lender’s perspective, credit scores at 740 and above will receive the best rate and term. A score of 800 will receive the same rate and term with a score of 740. Every twenty point increment will receive different rate/terms. Generally, lenders look for a minimum score of 620 (with some going as low as 580). The interest rate and the terms associated with a 620 score will be substantially different than a score of 740+. Basically, the higher the credit score, the monthly payment will be lower and the cost to administer the loan will be lower as well. This could save the borrower thousands of dollars over the life of the loan.

It’s not uncommon to have clients frustrated when a mortgage lender pulls their credit only to find their scores are substantially different than what they thought it would be. The scoring algorithms used by the automotive industry and “free” credit report sites are different from the mortgage industry. Nearly all lenders use FICO scores.

There are two main competitors in the credit scoring industry, FICO and VantageScore. FICO used to stand for Fair Isaac Company. Since then it was shortened to its official name, FICO. FICO’s biggest competitor is VantageScore and is gaining traction. It was developed in 2006 by the three major bureaus. Both use proprietary algorithms to determine credit scores. VantageScore tends to provide scores relative to what have you done for me lately. FICO is in the process of tweaking their scoring to reflect what’s happening today as well but this will take time to integrate new methods of scoring.

Fannie Mae and Freddie Mac are key players who provide a guarantee for a portion of each loan administered by lenders. Freddie Mac and Fannie Mae endorse FICO scores and therefore lenders will follow suit to Fannie and Freddie guidelines including the use of credit scores.

FICO utilizes three credit bureaus, Experian, Equifax, and Transunion for score reporting and inf ormation. Each bureau evaluates your score differently and all three scores are typically different. From the three scores, lenders will drop the high and low score, and use the middle score or qualifying score to determine your actual credit score for loan qualifying purposes. If there is more than one borrower, the lowest mid score will be used.

ormation. Each bureau evaluates your score differently and all three scores are typically different. From the three scores, lenders will drop the high and low score, and use the middle score or qualifying score to determine your actual credit score for loan qualifying purposes. If there is more than one borrower, the lowest mid score will be used.

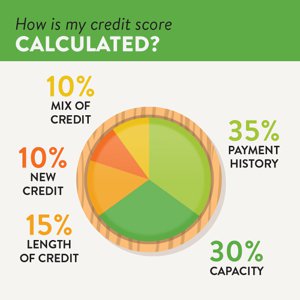

Scores range from 300 to 850 with FICO. Credit scores are generally based on the following breakdown:

If you don’t have the time to improve your scores, there are credit repair companies for hire that can guide you through the process. They will monitor your credit behavior, work with you on disputes, and provide helpful hints to bolster your scores. Most companies charge around $100/month. Another alternative is to work closely with your loan officer who specializes in credit restoration. By examining your credit report, we can easily spot areas for improvement and provide helpful hints. Most often, none of these tips are industry secrets. You can also do it on your own. If you decide on this path, make sure your scores are driven from FICO and your scores and credit history are reported from all three bureaus. No matter the direction, the best path is to do any of these in concert with a lender driven credit report.

![]()